By Infinium Global Research Aug, 2020

LNG bunkering is the practice of providing liquefied natural

gas to a ship for its own consumption. LNG is a cleaner fuel than conventional

marine fuels, such as heavy fuel oil, marine diesel fuel, and marine gas fuels.

Stringent government laws to reduce

airborne marine emissions that include pollutants such as sulfur and nitrous

oxide along with shifting trends towards clean energy are the major factors

driving the growth of the LNG bunkering market. In addition, LNG fuel has low

sulfur content and needs comparatively less processing to meet the sulfur

content limits and hence it will require smaller and less expensive modifications

compared to conventional marine fuels. For instance, the regulation passed by

the International Maritime Organization (IMO) in 2012, that stated, ships must

reduce their sulfur content in fuel from 4.5% to 3.5%. However, higher capital

investments and poor bunkering infrastructure are the factors, anticipated to

restrain the growth of the LNG bunkering market during the forecast period.

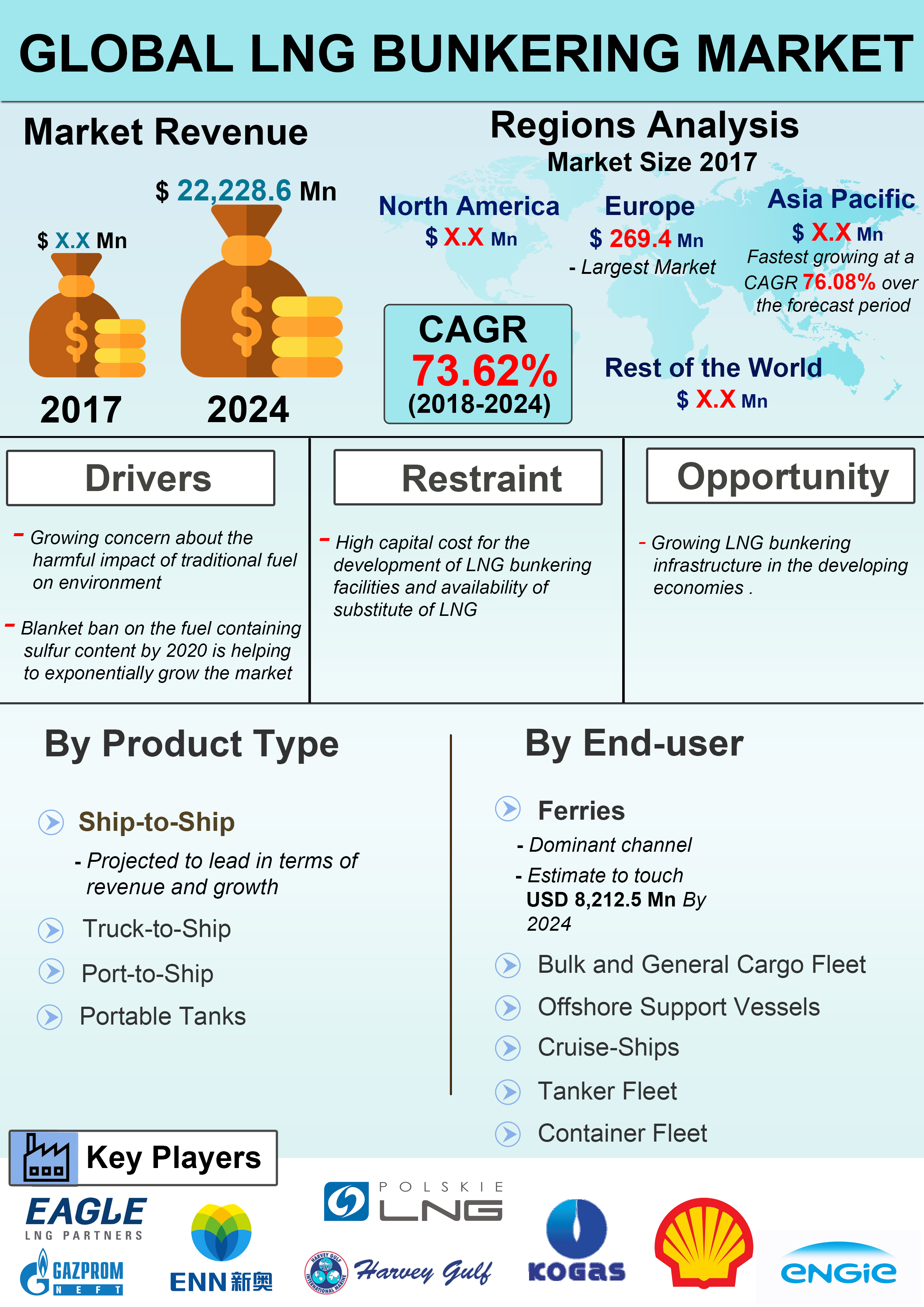

The report on Global

LNG Bunkering Market covers segments such as product type and end user.

The report provides regional analysis covering geographies such as North

America, Europe, Asia-Pacific, Rest of the World. In this section, the key

trends and market size for each geography are provided over the period of

2016-2024. The report provides profiles of the companies in the global

Gazpromneft Marine Bunker Ltd, ENN Group, Eagle LNG Partners, Polskie LNG SA,

Harvey Gulf International Marine LLC, Korea Gas Corporation, Skangass AS, Royal

Dutch Shell PLC, and ENGIE.